In last week’s blog on liquidity risk in high yield and fixed income, we discussed Third Avenue’s recent lock-up and why liquidity is a concern now, more than ever. At Bramshill Investments, we manage absolute return solutions in fixed income and income producing assets. In our investment process, liquidity matters, and we believe the liquidity issues in the market place today tip the odds in favor of smaller firms. Below we share some of our market insights around these liquidity risk factors which many advisors may be overlooking in their due diligence of fixed income managers.

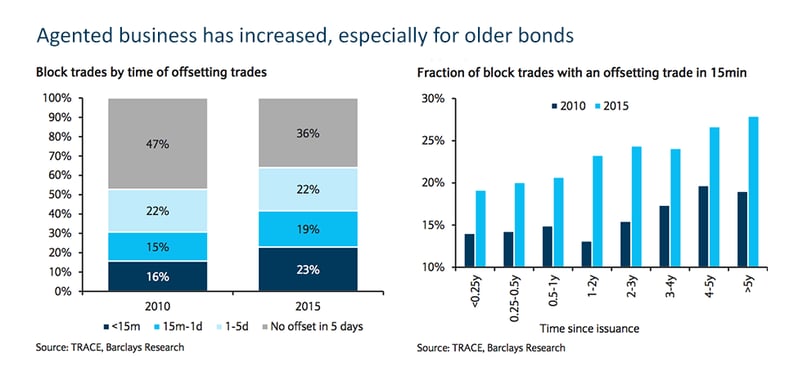

Due to regulation, somewhere between 45-65% of all bond trades are done on an agency basis:

The trend isn’t stopping anytime soon as regulation continues to come into action (new US rule under Basel guidance). Couple the regulatory changes with an increase in electronic bond trading and fixed income managers now face wider bid-ask spreads and smaller average transaction sizes. This phenomenon allows players who are more nimble and transacting in smaller sizes to get better pricing; the ability to move blocks of $25MM+ will become more difficult and more costly. In times of stress, this theme of liquidity risk will be exacerbated.

Missed our recent intro conference call? Listen to the replay!

Stephen Selver is the CEO at Bramshill Investments, an asset management firm specializing in absolute return solutions within fixed income and income producing assets. Click here to view his bio and other team members of Bramshill Investments.

Stephen Selver is the CEO at Bramshill Investments, an asset management firm specializing in absolute return solutions within fixed income and income producing assets. Click here to view his bio and other team members of Bramshill Investments.